The following has been adapted from a presentation delivered at Commonfund Forum 2023. The presenters were Rachel Stavola Clivaz, Associate Director, and Anthony Peretore, Managing Director, Commonfund OCIO; and Allison Kaspriske, Director, Commonfund Institute.

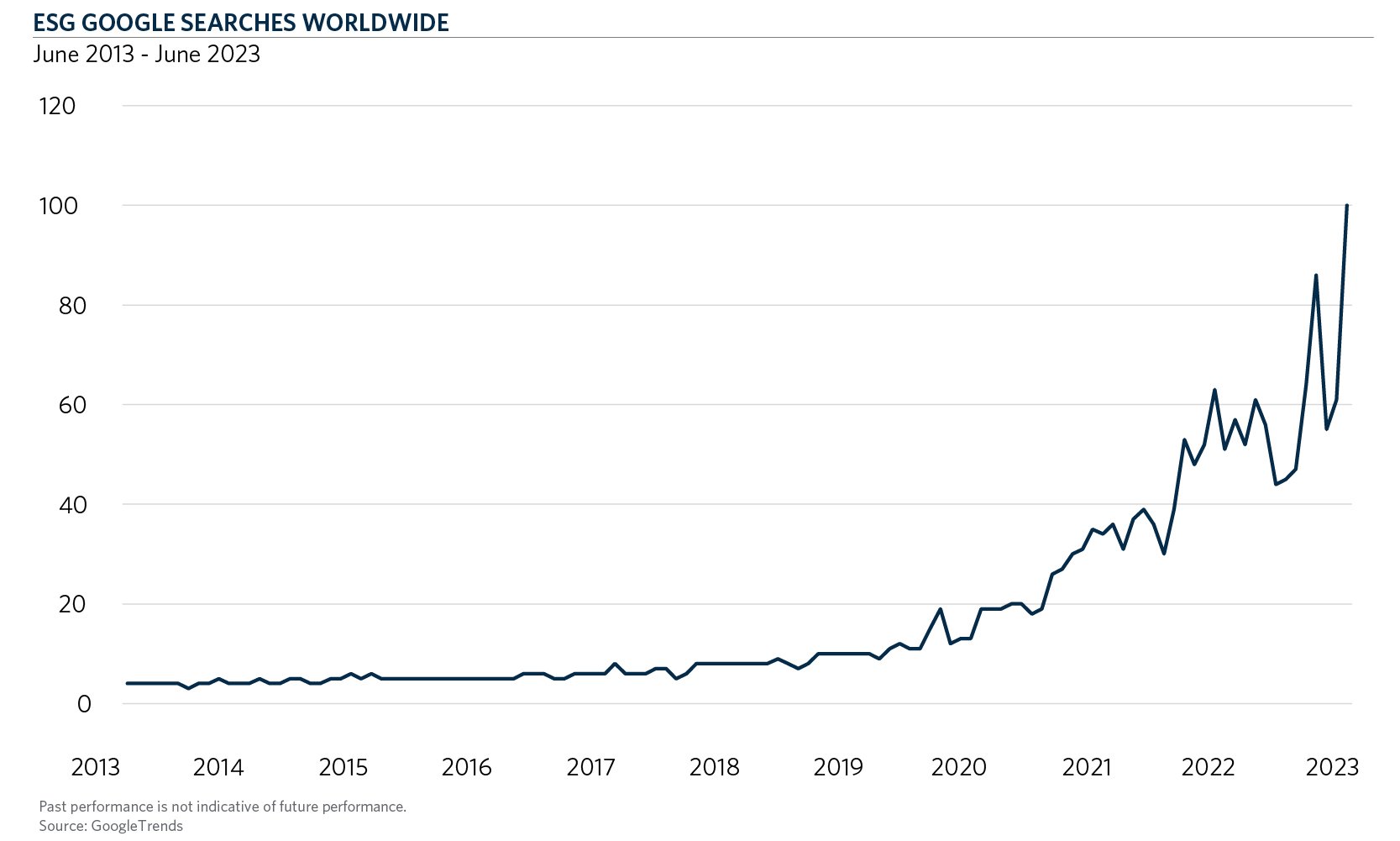

Over the past few decades, responsible, or ESG (environmental, social, governance), investing has transformed from margin to mainstream and continues to receive increasing levels of attention across all corners of the asset management industry, including nonprofit investors. One way to demonstrate that growth in interest comes from Google searches for “ESG” over the past 10 years:

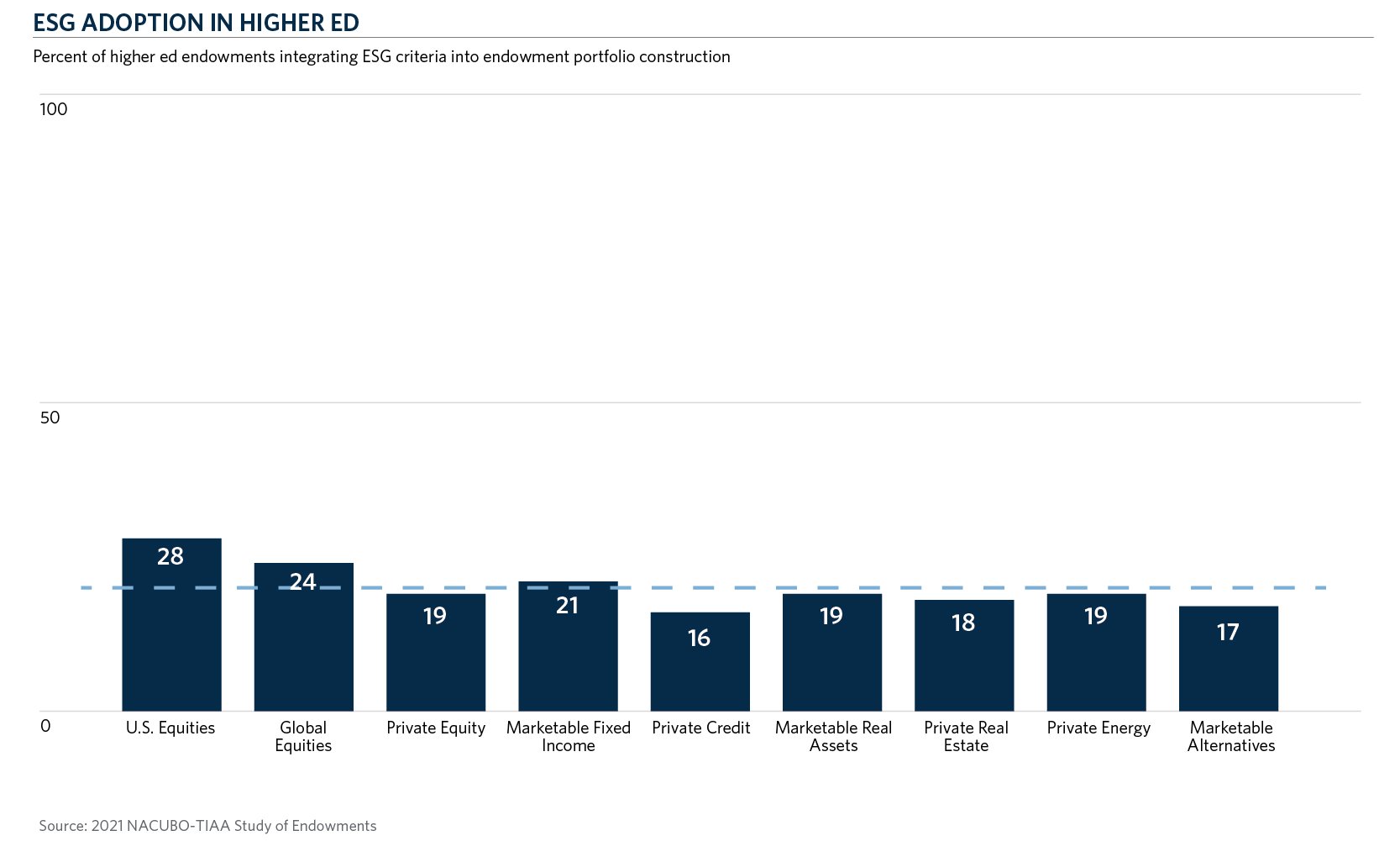

However, while interest in ESG investing has certainly gained momentum, adoption of ESG criteria within nonprofit portfolios has not grown commensurately. The example below shows that on average, roughly 20 percent of endowments (dashed blue line) from the latest NACUBO-TIAA Study of Endowments are incorporating ESG criteria into their portfolios.

So, why the dislocation between interest and action? The primary reasons we have found through our research and data collection include:

- Difficulty assessing the degree of success in achieving an ESG mandate

- Insufficient opportunity set offered by ESG investments

- Potential for adverse impacts on performance

- Potential conflict with mission

- Potential increase in fees

Further, based on our own experience with our OCIO clients, another sizable hurdle remains a lack of guidance, or structure, on how to appropriately consider ESG integration for an endowment and institution. That’s why over the past several years we have prioritized the development of a responsible investing framework to help our clients make meaningful progress toward their ESG integration goals.

That framework is structured as a three-step process for moving from ESG consideration to implementation:

Education

Prior to any discussions around ESG integration, it is important to first ensure that all fiduciaries and staff have a common understanding of what is meant by ESG and how that criteria is being considered within the management of the endowment. Our focus tends to be on:

- Broad definitions of E, S and G

- Why ESG warrants consideration, among other factors, within the investment process

- How Commonfund is integrating ESG within its investment process

- How Diversity, Equity and Inclusion (DEI) fits into this discussion and in the broader mandates of the endowment, as well as at Commonfund

- Does the current portfolio (or the processes behind portfolio construction) already include some elements of ESG? If so, what are they?

- How does this compare to what peers are doing as it relates to ESG – in the endowment, on campus, in the community, etc. ?

| Environmental | Social | Governance |

|

|

|

| Source: PRI | ||

Integration

Following the educational discussions, we then transition into the integration phase. This phase has two primary areas of focus: (1) an anonymous ESG survey, and (2) the introduction (or review) of our ESG integration framework.

The survey, developed by Commonfund over time (and consistently refined as ESG continues to evolve), seeks to gather the views and preferences of the committee members related to the key, institution-specific ESG considerations, including:

- The areas of ESG (and DEI) they would like to prioritize in the endowment

- Preferred metrics to track progress over time

- How they believe ESG should be captured in the Investment Policy Statement (IPS) and communicated to other stakeholders

This tool is useful not only because it provides Commonfund clarity around the scope of (potentially) varying opinions on ESG, but it also allows the committee and staff to gauge each other’s opinions, while doing so in an anonymized format. Ultimately, this helps provide a foundation for future conversation topics and explorations and, importantly, how to transition into the initial stage of ESG integration.

For the latter, we use a proprietary framework centered around integration in three main areas: investments, analytics, and governance and communication. For each of these areas of focus, there are three different levels, or tiers, of integration, as shown in the framework below, with higher tiers representing increasing levels of integration.

Our primary goal with this framework is to help the institutions we partner with evaluate which level of integration is most appropriate for them within each of these verticals. Importantly, it is not necessary for an institution to be at the same level of integration across all three verticals, as the approach to ESG should be tailored to what best fits the needs of an institution. For instance, a committee may elect to take a more standard approach to investment integration (e.g., Tier 1) but a more proactive approach with IPS language and/or communication (e.g., Tier 2).

Further, we also express to our clients that the initial goal should not necessarily be to strive for a higher tier of integration, but more on determining what the most appropriate tier is for their institution at this point in time. Given that many investment committees are now reviewing the topic of ESG on an annual basis, we can consistently revisit which tier is best for an institution, which may change over time. The primary reasons we see for clients shifting into a higher tier include:

- Greater comfort with ESG and its role within the investment process

- Increasing interest on campus or in the community, and/or new initiatives that encourage the endowment to further consider ESG

- Evolving sentiments on more targeted ESG adoption driven by potentially differentiated views of new trustees, committee members and/or senior leadership at an institution

Evaluation

Once the education and integration discussions conclude, we need to periodically assess whether trustees and staff are still properly educated around ESG and its role in the endowment, including whether the optimal tiers of integration are still in place. This ongoing evaluation typically includes regular ESG agenda topics at investment committee meetings, as well as continued dialogue with staff, particularly around any recent developments related to ESG and the institution. Further, we often find it important to speak with other stakeholders and/or trustees to capture the sentiment around ESG from a broader audience. An example of questions we may seek to answer:

- What is it that the community wants to hear about ESG and the endowment?

- In your opinion, is the endowment appropriately considering ESG?

- How can we communicate effectively and engage with a broader audience?

Conclusion

In summary, our experience shows that a systematic approach built around clearly defined, discrete steps can help overcome the hurdles associated with a successful ESG implementation—and close the gap by moving ESG from interest to integration. The tailored approach to our framework allows our clients to appropriately consider ESG for their institution and adopt an integration plan that aligns with their preferred pace and scope.