In today’s environment, commentary can seemingly become stale in periods as short as hours, let alone days. Just last month, we wrote how despite tightening lending conditions from banks, other metrics of financial conditions such as Goldman’s Financial Conditions Index or the ICE BofA MOVE Index had been signaling easing financial conditions and moderating volatility. More importantly, the bond market itself had been pricing the forward rate curve with expectations (and likely hopes) of easing.

However, by early March, a combination of hot economic data and hawkish rhetoric from Fed Chairman Jerome Powell resulted in another sharp upward repricing of bond futures and dashing hopes for near term relief from tighter monetary policy.

Expectations for “higher for longer” central bank rates were quickly dampened a week later. The financial world was disrupted as Silicon Valley Bank (SVB) announced a multibillion-dollar loss on their held-to-maturity securities which were sold to cover mounting deposit outflows. SVB was taken into FDIC receivership in the morning of March 10th. In response, U.S. Treasury yields fell sharply driven by investor fears of contagion and a flight to quality. The 2-year U.S. Treasury bond yield dropped nearly 30 basis points that day and another 60 basis points on March 13th, which in aggregate was the largest daily change since the early 1980s. Financial conditions appear to have tightened significantly in only days and rates volatility has reached new cycle highs (the MOVE Index has surpassed its COVID period high and approached its 2008 peak). As a result, forward rate expectations have been in constant flux over the past two weeks.

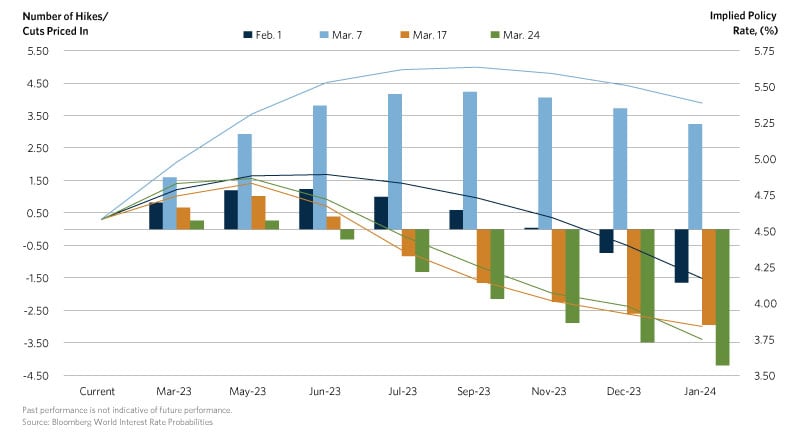

This Chart of the Month depicts the market implied forward Fed Funds curve on four dates: February 1st, March 7th, March 17th, and March 24th. Very clearly, there has been little continuity in forward rate expectations over the past six weeks. Forward rate hike pricing has come full circle from a peak in June 2023, to higher-for-longer hiking cycle with a peak in September, and now back to pricing rate cuts as soon as the June Federal Open Market Committee (FOMC) meeting. The shifts have been drastic: expectations for the terminal Fed Funds Rate increased over 70 basis points from 4.9 percent to nearly 5.7 percent as of March 7th but have fallen precipitously to 4.75 percent (only one more hike expected) as bond investors anticipate a Fed pivot due to concerns of financial instability. Perhaps the most striking shift is that the implied Fed Funds Rate in January of 2024 has shifted downward over 160 basis points in just 9 days.

Despite the whirlwind of news in the last two weeks, one factor has remained constant: inflation is still running well above target and is unlikely to slow in a linear fashion as many had hoped. As goods pressures have cooled, the focus remains on core services and wage pressures that have only slowly moderated. The much-anticipated slowdown in non-farm payroll growth has yet to occur, with the February print crushing expectations for the 11th month in a row. The resulting 25 basis point hike on March 22nd did not come as a surprise, but market expectations have diverged significantly from those outlined in the Fed’s Summary of Economic Projections. At present, the market-implied Fed Funds Rate (~4 percent) by December 2023 is 110 basis points lower than the median expectation of the FOMC. While the FOMC is signaling perhaps one more rate hike and a clear pause, markets have yet to give credence to their sentiments. Amid rampant uncertainty, the margin of error for Chair Powell and the Open Market Committee has narrowed even farther than many expected.