At Commonfund, we scour the globe to find investment managers that we believe have the ability to consistently produce excess returns (alpha) over and beyond their benchmark. But alpha alone is not enough. We also dig deeply into the sources of those returns to understand the underlying factors driving the strategy. Through our construction process we look to combine uncorrelated sources of return, thereby reducing overall portfolio risk. This search for uncorrelated alpha sources requires finding managers that are different from the crowd.

One byproduct of this effort has led to a history of investing in women and minority-owned managers in both Commonfund commingled programs as well as customized mandates, including within our hedge fund and private equity programs.[1] In recent years, however, this search for diverse managers has become a more formalized initiative. Drawing on a proprietary database of managers and a clearly defined institutional due diligence process, women and minority manager searches are now intentionally incorporated into every traditional equity and fixed income manager search at Commonfund.

For some clients, reasons for incorporating diverse managers in portfolios tend to start with efforts to create a positive social impact and to address socially-driven economic imbalances. Many of our endowment and foundation clients, as well as a number of public pensions have been vocal supporters of adding diverse managers on these grounds. But there are other compelling reasons to consider incorporating diverse managers in your portfolio.

The first of these is the simple benefit of diversity itself. Endowments and foundations have long understood the value of diversity of asset classes in their portfolios to help portfolios weather market vagaries. Many are also aware of a growing body of academic work that demonstrates the value of diversity in teams in generating smarter, more creative outcomes.[2] The implication for asset management is that investment teams that are diverse in background, gender and ethnicity also offer opportunities to generate better investment outcomes.

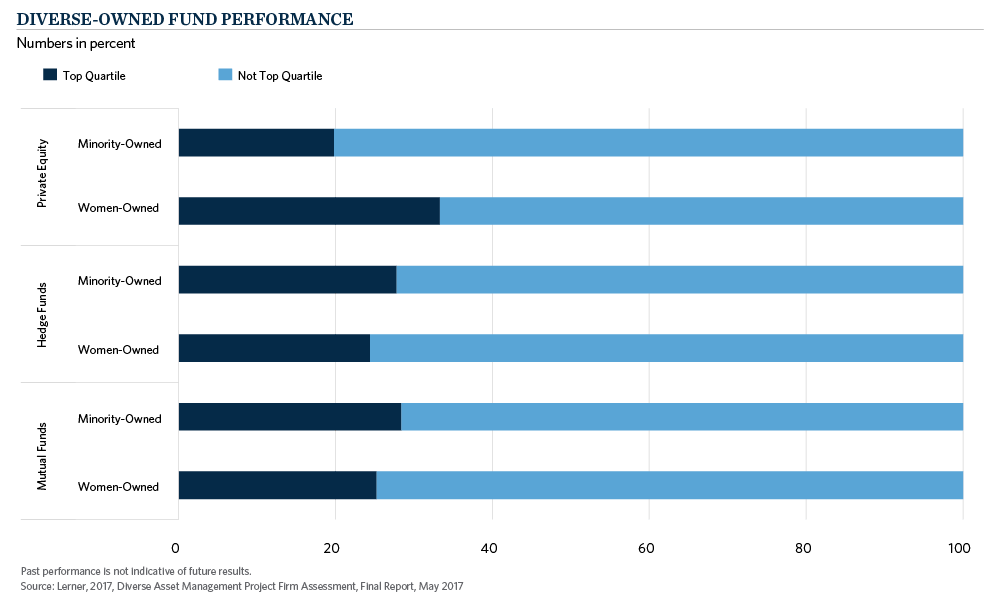

Secondly, embedded in most investor’s assumptions is that there is a performance cost to investing in diverse managers. However, the math suggests we should not ignore the performance opportunity women and minority firms offer. Although databases for diverse managers vary in quality and size across asset classes, a study commissioned by the Knight Foundation, and led by Josh Lerner at Harvard Business School and the Bella Research Group, demonstrates that there is no statistical difference in performance between diverse-owned firms and their peers.[3] Their study demonstrates that 20 percent or more of all women and minority owned firms fall in the top performance quartile of their respective investment strategy peers.

But there are challenges. In addition to the obvious difficulties faced in all manager searches, of finding those top quartile performers, the diverse manager universe forms only a small subset of the total managers within each asset class. With fewer managers to choose from, the sheer number of managers in the top quartile is necessarily limited.

Moreover, performance is not the only criteria for manager selection. Institutional operational standards are often cited as a barrier to investing in small or emerging managers and it is unquestionably true that the expense of establishing a strong operational platform is greater today than ever before, with more staff required to cope with additional regulatory requirements and client requests. Often the asset size of the manager itself is a hurdle and becomes a self-fulfilling prophecy when many consultants and investors judge these managers too risky due to limited size and resources.

We believe these challenges can be overcome. Concerted efforts to remain current with the investment universe and opportunities is paramount. If you do not look, you are certainly less likely to find. In addition, barring a minimum asset size capable of paying for basic operational services, high quality outsourcing services such as compliance, risk analytics and trading can help mitigate most of the operational hurdles to institutional investment.

Visit our Commonfund website today to learn more about responsible investing.

[1] Minority investments generally include women and racial and ethnic minorities including African American, Latino, Asian and Native Americans and may also include veterans and people with disabilities.

[2] Herring, Cedric. 2009. “Does Diversity Pay?: Race, Gender, and the Business Case for Diversity.” American Sociological Review.

Orlando, Richard C. 2004. “Racial Diversity, Business Strategy and Firm Performance: A Resource-Based View.” Academy of Management Journal.

Phillips, Katherine W. 2014. “How Diversity Makes Us Smarter.” Scientific American.

[3] Lerner, Josh Harvard Business School and The Bella Research Group. 2017. Diverse Asset Management Project: Firm Assessment. The John S. And James L. Knight Foundation.