Environmental, social and governance (ESG) factors are a topic for active discussion in board rooms. Here’s an update on Commonfund’s thoughts and actions and how ESG may relate to you.

In general, ESG is used to describe a group of characteristics that can have a material impact on the long-term success of a company and, potentially, investment returns. Examples of the “E” in ESG criteria include environmental factors, such as energy consumption and greenhouse gas emissions; examples of the “S” include social factors, such as supply-chain risk management, corporate citizenship, gender and racial diversity, and employee productivity; examples of the “G” include governance factors, such as independent board leadership and CEO compensation.

Classic portfolio theory holds that if securities are excluded from a portfolio for reasons other than expected return, the resulting portfolio may be suboptimal, either in terms of risk or returns. However, in certain instances, ESG issues can have a material impact on the investment thesis for a particular company and, thus, should be factored into investment decision-making.

Research as to whether ESG factors have an impact on portfolio returns is still emerging. However, academic studies overwhelmingly support the thesis that integration of ESG factors into an investment process has a positive impact on portfolio performance. A growing body of research suggests that, all other things being equal, companies with higher ESG ratings tend to outperform their peers in times of economic duress and are more resilient in the face of high-impact, low frequency risks (so-called fat tail risks).

Commonfund's ESG perspective

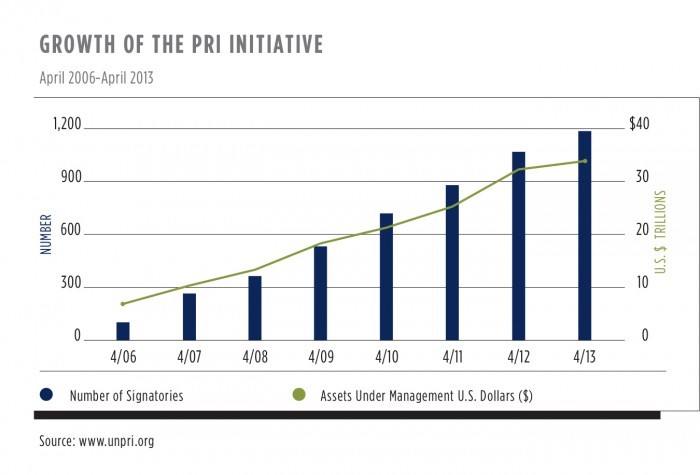

At Commonfund, we view ESG criteria as one set of factors among many that should be weighed appropriately to inform investment decision-making. Commonfund’s investment programs are designed to generate superior long-term investment performance net of fees and enhance the financial resources of long-term institutional investors. We recognize that ESG factors may have a material impact on long-term investment performance. Consistent with this belief, Commonfund analyzes ESG factors as part of its fundamental investment analysis process. While research is increasingly showing positive benefits from the consideration of ESG factors, we recognize that there is still more to be done to understand which ESG factors are material to which investment strategies. In becoming a signatory to the Principles for Responsible Investment (PRI), we joined a network of 1,200 international investors and asset managers working together to put the six Principles into practice. The Principles were devised by the investment community and reflect the view that ESG criteria can affect the performance of investment portfolios and, therefore, must be given appropriate consideration by investors if they are to fulfill their fiduciary (or equivalent) duty. The Principles provide a voluntary and flexible framework by which all investors can incorporate ESG factors into their decision-making and ownership practices.

Among specific actions, we have added questions about our investment managers’ ESG practices as part of our due diligence process. (Please refer to page 6 and the discussion of “monitor, measure, manage” for more on this topic.) We also serve on the Advisory Council of the Sustainability Accounting Standards Board, contributing to the development of materiality standards for public company reporting purposes. Commonfund also serves on the PRI Private Equity Working Group and, in that capacity, helped to create a guide for the general partners of private equity funds that outlines best practices in ESG implementation.

Has becoming a signatory changed our investment process? Commonfund’s ESG efforts are informed by a working group with representatives from each investment team and our sales, risk, legal, trading and RFP teams. Commonfund does not exclude particular industries, geographic regions or strategies based on ESG factors; rather we take ESG factors into consideration as part of our fundamental investment analysis in instances where such factors have the potential to impact the value of our clients’ investments.

PRI's six principles for responsible investment

| 1 |

Incorporate ESG issues into investment analysis and decision-making processes. |

| 2 |

Be active owners and incorporate ESG issues into ownership policies and practices. |

| 3 |

Seek appropriate disclosure on ESG issues by the entities in which we invest. |

| 4 |

Promote acceptance and implementation of the Principles within the investment industry. |

| 5 |

Work together to enhance our effectiveness in implementing the Principles. |

| 6 |

Report on our activities and progress towards implementing the Principles. |

Position on divesting fossil fuel investments

Divestiture of fossil fuel investments has received a great deal of attention. We believe that the decision regarding divestment is particular to each institution and each will need to go through its own process to determine the right action to take regarding this issue.

Commonfund is concerned about the impact of potential stranded assets (assets that become prematurely obsolete or non-performing due to environmental liabilities) on our portfolios and is in the process of looking more closely at how this can impact our clients. We are evaluating strategies to address any increased risk, which includes working closely with Commonfund’s Board Chair, Robert Litterman, who has written extensively on pricing carbon risk.

On the marketable side, we have identified which of our portfolios hold any of the 200 companies identified by 350.org (an environmental organization with the goal of raising awareness about climate change) and are reaching out to our managers with the highest concentrations of investments in those companies to talk with them about the stranded assets risk. On the private capital side, we note that our natural resources funds have little coal exposure, with more concentration in lower carbon-intensive fuels. Two of our mining managers are PRI signatories and this is a topic on which the investment team regularly engages its managers.

Preliminary studies have shown that the impact of divesting from the 200 companies identified by 350.org is small to negligible on portfolio performance and risk. A few points Commonfund believes are important to consider are:

-

Divestment means giving up the opportunity to engage companies as shareholders and push for improvements in practices, investments in new technologies, etc.

-

Portfolios that have divested from the largest 200 fossil fuel companies may have a higher carbon footprint than portfolios that try to lower their carbon footprint across all companies (rather than focus on particular industries).

The Principles for Responsible Investment provide a voluntary and flexible framework

by which all investors can incorporate ESG factors.

Implementing ESG at your institution

What should individual institutions considering ESG implementation think about? Two actionable steps that your institution might consider if you are starting your ESG journey are, first, defining what ESG means in the context of your organization. An institution’s definition of long term (investment horizon), where its operating exposures are and what its mission is may help determine which ESG criteria are most material for its investment portfolio. Second, whether an institution wants to go beyond ESG to a more targeted approach, such as impact investing, will depend on what responsible investing means to the institution. Fundamentally, investors must decide if particular environmental, social or governance issues are sufficiently important to their stakeholders and beneficiaries that they are interested in targeting their investment choices.

Institutions considering implementation of ESG may want to consider some of the challenges that Commonfund encountered in its early experiences as a signatory to the PRI. We have found challenges to be in three areas:

-

Importance of being specific – It is important to be specific when talking about ESG. There is a broad universe of criteria and issues that fall under these categories and whether they are relevant to be considered in an investment analysis varies across asset class, strategy, industry and geography. The process of determining which issues are material to which investments is fact-specific and labor-intensive.

-

Battle of the metrics – There is a wide array of metrics for measuring the materiality of these factors and each system has its own pros and cons. Various proprietary manager metrics can be applied. It is important to sort through them and determine which metrics work best for various purposes.

-

Wide dispersion across managers European managers are further ahead in implementing ESG considerations in their portfolios than U.S. managers; generally, natural resource and private equity managers are ahead of hedge fund and fixed income managers.

It may also help institutions to think in terms of monitoring, measuring and managing. Again, based on our experience at Commonfund, here is a summary of our actions in each of these areas:

-

Monitor (manager due diligence) – ESG considerations are reviewed alongside more traditional indicators such as team, strategy, performance and terms of investment. As part of Commonfund’s due diligence process we ask potential managers a series of questions about whether and how they integrate analysis of financially material ESG factors into their investment process.

-

Measure – We conduct periodic and targeted reviews of our portfolios to assess their exposure to ESG-related opportunities and risks and are in the process of refining our approach to this aggregate portfolio analysis across all of our portfolios.

-

Implement/Manage – In addition to the manager due diligence process described above, once a manager has been approved for investment, Commonfund may endeavor to negotiate provisions with the manager addressing whether and how ESG factors will be reflected in the construction of the portfolio; reporting on the impact of ESG factors within the portfolio; proxy voting; and any targets relating to ESG integration. We are undertaking our own original research to continue to evaluate the investment merits of ESG factors and the most effective methods to address these issues.

Institutions considering their own ESG initiative may want to remember

three key steps—monitor, measure and manage.

Defining differences: ESG, SRI and Impact Investing

Sometimes there is confusion surrounding the differences between three types of responsible investing—ESG, socially responsible investing (SRI) and impact investing. Each falls under the broad heading of responsible investing, but each serves a very different purpose.

SRI

SRI mandates typically incorporate screens for certain social and environmental issues based on an institution’s moral, ethical or religious beliefs. Investors engaging in SRI may eliminate entire sectors, companies or even countries from their investment universe regardless of the impact on portfolio performance and risk.

ESG

In contrast, ESG integration means evaluating and considering various ESG criteria during the investment process only to the extent those criteria may be material to investment performance. ESG integration recognizes that context matters and that the risks and opportunities posed by ESG factors can vary greatly depending on geography, industry and asset class. In some respects, ESG is a grouping of previously existing investment perspectives. Environmental factors, governance factors, and social factors have long been part of the mosaic approach to investment analysis. ESG integration can also lead investors to engage with companies that have poor policies around environmental, governance and social issues in an effort to improve them, whereas an SRI approach might just lead to screening such companies out of a portfolio.

Impact investing

Impact investing is a more affirmative strategy in which institutions choose to target their investments to effect specific environmental or social change, such as investing in economic development zones or social entrepreneurs. Sometimes the potential social impact can take precedence over returns as the primary driver of investment decisions.