Active management has struggled for several years, raising questions about whether active management can ever outperform again. Traditional active manager style tilts, like value and size, have detracted from performance in recent periods.

Over the long run, these tilts tend to mean revert around positive trends, creating reasons to be optimistic about active management’s prospects. On the other hand, only 30 percent of managers truly deliver positive alpha after controlling for typical active management style tilts. Fortunately, the average manager who has delivered alpha in the past tends to deliver meaningful positive alpha in the future. A strategy of quantitatively identifying managers who have delivered alpha in the past, putting them through additional rigorous due diligence processes and incorporating proven style tilts into the overall portfolio design offers substantial promise.

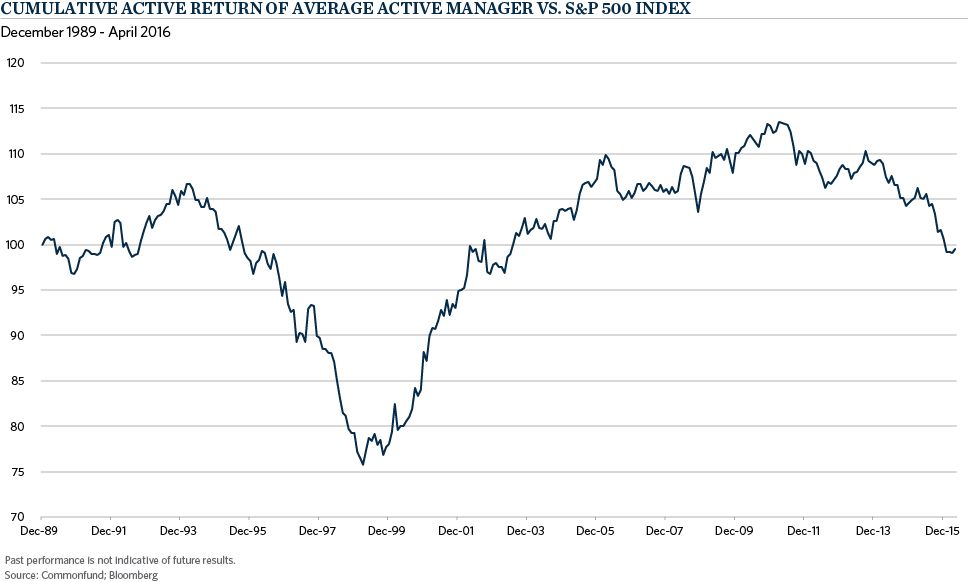

Active management fatigue anyone? Disappointing performance in active management has persisted for four years now. The chart below depicts the cumulative active return of the median active equity manager benchmarked to the S&P 500 in the Bloomberg Universe.[1] It shows a clear and worrisome downturn beginning towards the end of 2011.

Throughout the full history since 1990, however, the median active manager has performed in line with the benchmark. Hardly a resounding endorsement, admittedly. And there are earlier periods, such as the mid-1990s, when active management struggled also. But there are also extended periods where active management has done quite well such as immediately after the mid-1990s. Indeed, the period from 1999 through 2010 was largely positive for active management, more or less continuously.

Can active management still do well? To answer this question, we need to better understand why it has underperformed. There are a host of stories that have been advanced by financial pundits including the growth of passive investing, the growth of ETFs, federal fiscal policy, central bank monetary expansion, increased market efficiency, the use of leverage, high frequency traders, hedge funds … and that is just getting started. Rather than try to test these qualitative hypotheses, we are going to look instead at the primary drivers of an active manager’s active return. We will let the pundits tie the conclusions of our analysis to their preferred explanation.

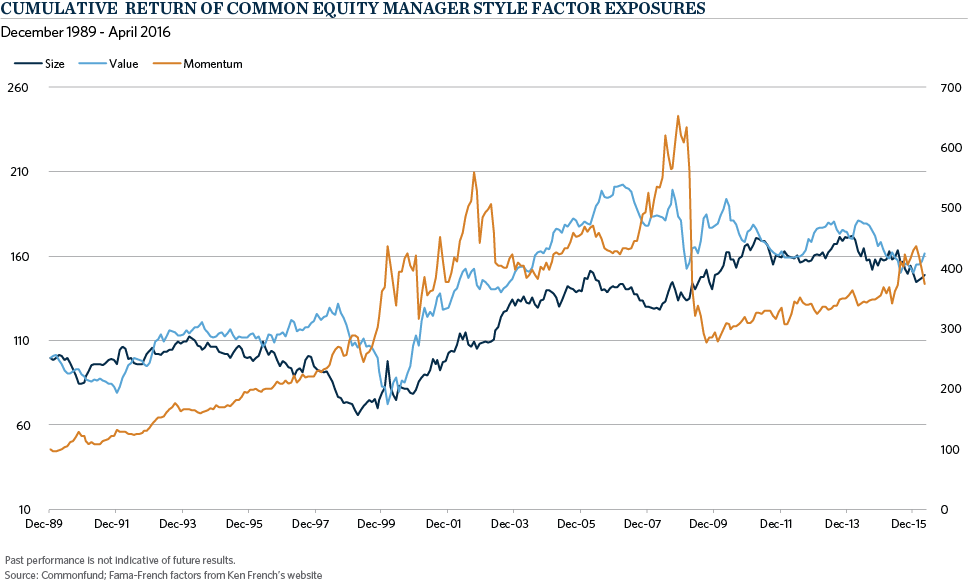

An active manager’s return versus his or her benchmark can be decomposed into two pieces: alpha and systematic risk (or beta). Alpha is true skill, the rarest of attributes. Systematic risk is more mundane but tends to be rewarding over long periods of time. The most familiar form of systematic risk is equity market beta. But active managers know a few other forms of systematic risk that can add to risk-adjusted returns over time. These include size, value and momentum. Size reflects the finding that small company stocks tend to outperform over time; value reflects the finding that companies priced inexpensively relative to their book value tend to outperform over time; and momentum reflects the finding that stocks that have done well in the recent past tend to continue to outperform. Size, value and momentum are three examples of what are commonly called style factors.

Bad style factor bets have been partly responsible for active management’s recent troubles. Value and size have not done well for five years now and quite poorly for the last two years (although we may be seeing an incipient upswing). Even momentum has done poorly since the start of the year.

Nonetheless, style factor bets have added value long term and, as evident from the chart below, do have a tendency to mean revert around an apparent upward trend. Furthermore, some of the newer style factors related to quality (e.g., profitability and conservative investment) and low volatility, have held up better recently. This raises the question of whether those who fail to incorporate new ideas are the source of active management’s doldrums. At Commonfund, we believe firmly in the benefits of modest amounts of compensated style factor exposures. Thus, we look to keep style factor beta in our client portfolios as it helps over time.

The more important question when evaluating active managers, though, is manager alpha. Many managers masquerade as deliverers of alpha. Yet when their purported alpha is dissected carefully, it may be nothing more than systematic risk in the form of style factor betas. The most common example is, again, market beta. Consider a manager who generates a return of 12 percent when markets return 10 percent. One might be inclined to estimate that manager’s alpha as 2 percent. However, what happens when the market turns back down? If the market then drops by 10 percent, does the manager lose 12 percent? If so, the manager has a market beta of 1.2 and no alpha. There was no skill. Just more risk.

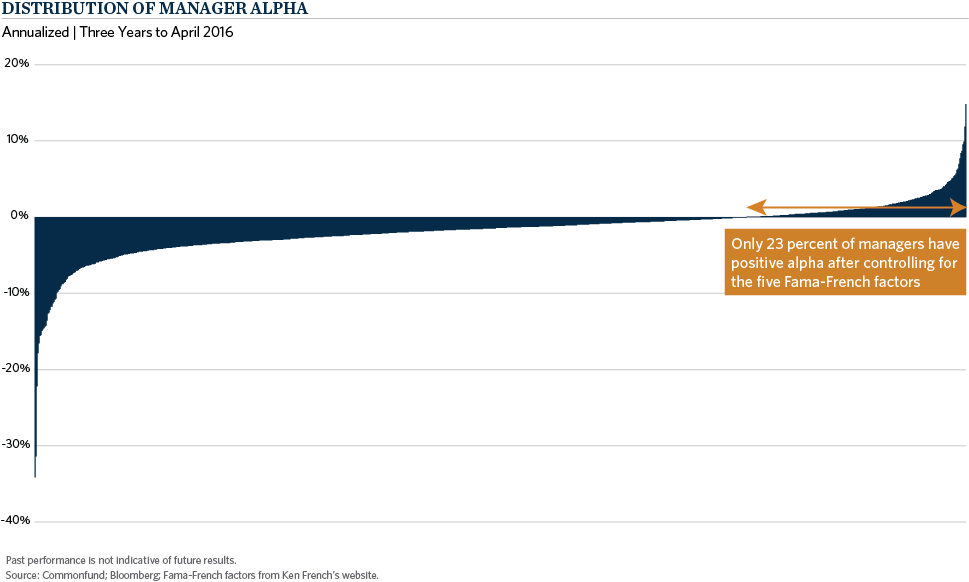

True alpha is scarce. After we control for systematic risk exposures in the form of style factor betas, 23 percent of active managers in the Bloomberg Universe delivered positive alpha over the past three years. This means that 77 percent of managers deliver negative skill after controlling for sources of systematic risk!

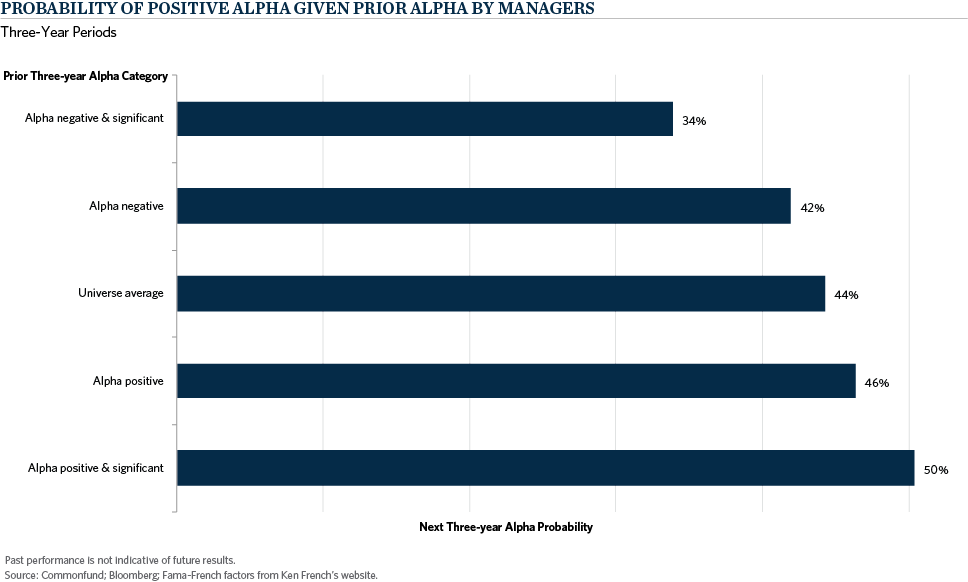

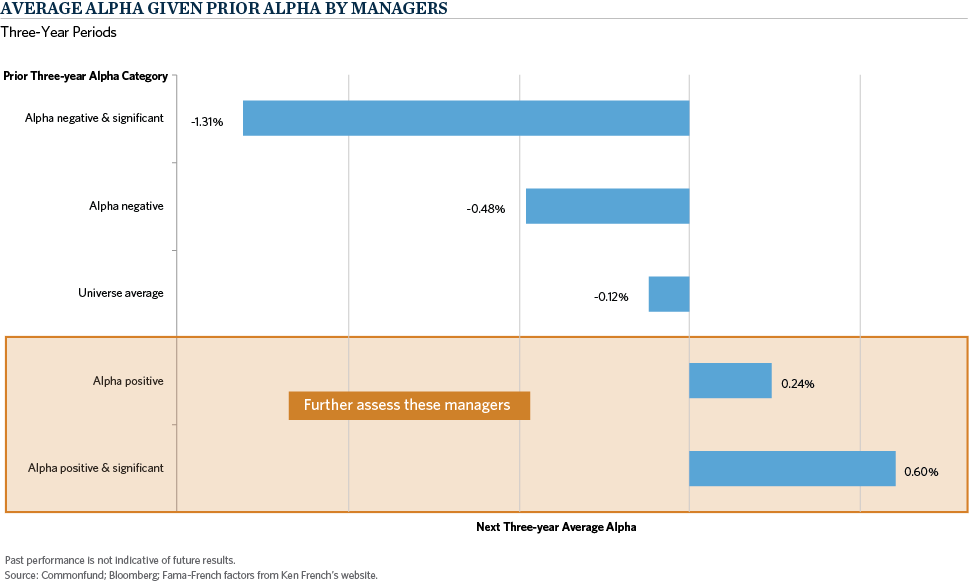

Yet what if we chose to focus on those managers that deliver positive alpha? Do managers that have generated positive alpha in the past tend to generate positive alpha in the future? Well, yes and no. But there is a bright silver lining. Managers that have not delivered positive alpha in the past are unlikely to deliver positive alpha in the future. Even managers that have delivered positive alpha in the past have only a coin flip chance of delivering positive alpha in the future. On first pass, these results are disappointing. One might be inclined to give up on active management altogether (or short the managers that have done badly in the past!).

Here is where we come to the silver lining. If we take the simple average alpha of the managers that have delivered positive alpha in the past (the two highlighted bars below), they continue to deliver positive alpha in the future. This is a very important finding. Equal-weighting positive alpha producers from the past generates positive alpha production in the future. This is true even if only half of the managers are contributing positive alpha. The reason is simple: those who generate positive alpha generate a lot of alpha and those who generate negative alpha do not generate quite so much.

So let’s go back to the question posed earlier in this paper: can active management still do well? We think this is the wrong question. Don’t chase active returns. Rather, focus on alpha management. Spend your time trying to find consistent alpha producing managers. Examine manager performance net of systematic risk exposures. Then further evaluate those managers rigorously using traditional manager due diligence techniques. And while you are at it, put some carefully constructed style factor beta in your portfolio through careful manager selection and portfolio construction. The style factor tilts won’t always work but they can make for a good tail wind over long periods of time.

- Active return is measured as manager performance net of fees and the benchmark. The performance of the full universe of actual managers may be worse than that represented in the Bloomberg data due to reporting biases. Poor managers may elect not to report creating a selection effect. Mean manager performance shows similar results.